(Tech) private credit doom impending: is it really that bad?

What is happening with private credit and how is it connected to the Saaspocalypse?

The rise of private credit: building $4Tn assets under management in 15 years

The 2007-09 financial crisis had long standing consequences in the financial industry, that trickled to the overall real economy, notably through changes in global banking regulations.

Two asset classes were significantly affected: real estate / mortgage lending, and long-term corporate loans. The first one is perhaps what most immediately impacted people’s lives, with larger equity requirements for individuals to buy homes and very limited options for developers to fund their projects, which, coupled with increased urban concentration, has left a global housing crisis with no end in sight. The second one, though, is the focus of this article: banks have almost completely withdrawn from long-term corporate lending. This has left an open space for private credit funds, that have developed flexible, varied strategies. However, given that their whole business model relies on charging management fees, promising high returns to investors and harvesting carried interest, they have tended to flock only into highly remunerated asset classes.

One particular type of loan that has proven attractive to private credit funds is financing buyout deals. With a simple and scalable origination and go-to-market strategy, by just targeting private equity funds instead of end borrowers, and a type of client whose incentives clearly align with their own, they quickly took over leverage finance, eroding the banks’ market share even further when interest rates hiked.

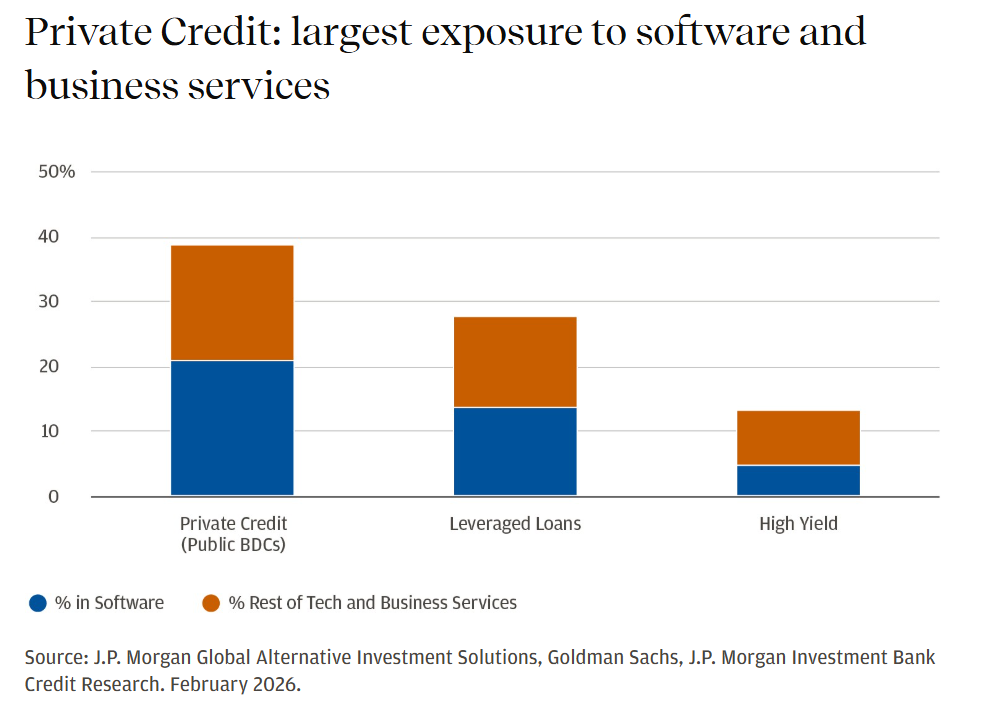

Within private credit, software and tech companies account for c. 20% of the exposure, and double that to include IT services. Some reasons for this overweight exposure are their lack of real, tangible assets that banks can use as collateral, and the assumption that recurring subscription revenue is very stable long-term cash flow. The exposure within leverage finance is slighly lower but also very relevant.

Source: https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/private-credit-under-the-microscope-separating-headlines-from-fundamentals (btw, highly recommend this article by JPM if you want to dig deeper, although their view is slightly different to mine)

So now that we know we have $4Tn in total private credit assets on the table (around $3.2Tn if you remove dry powder), of which close to $800Bn deployed on software borrowers, let us try to answer some questions.

What is really under the rug of credit funds?

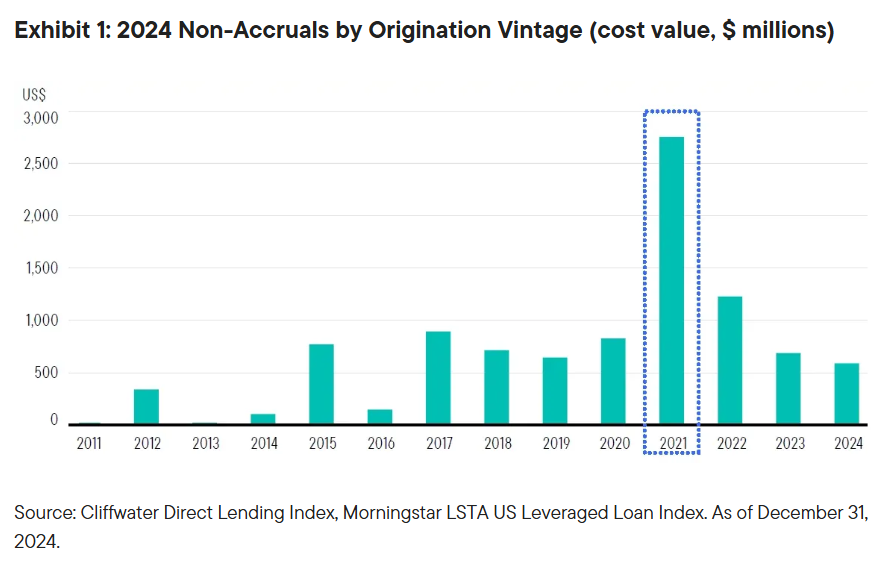

Something is already in the open and has been for a while: the 2020-23 vintages were ugly, and there is plenty of latent losses there. See the below chart and be aware that things have gotten notably worse since when it was published (data as of December 2024).

The very recent Medallia handover is only an example of what went wrong those days: buyouts of thin or no profit companies at more than 10x revenue, with deal leverage still being at 40-60%. The play during those years was hyper growth and hope for a 3-4 year exit to refinance all debt, which is a quasi-equity play, even more if you consider the structures on offer (PIK or cash/non-cash switch, bullet).

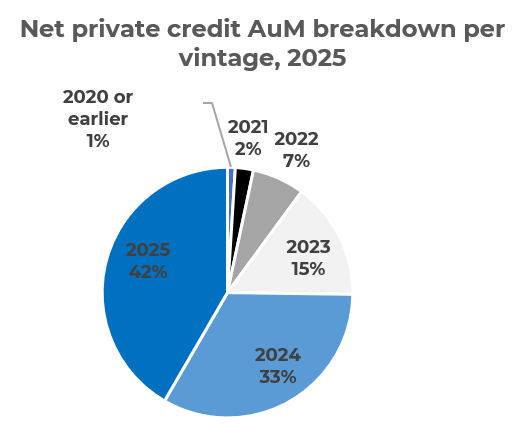

Is this a systemic threat to the private credit industry? The 2021 vintage is not, because deployment has grown significantly in recent years and 2021 represents a small fraction of current net assets under management. Below is my estimate vintage breakdown of current AuM (ex dry powder) as of today, based on the most recent ACC survey on AuM and deployment per year, with estimated repayments based on a c. 5-year average maturity.

The broader underwriting policies of leverage finance lenders have stuck to a 40-60% of EV, and given recent multiple contractions, I would expect the 2025 tech cohort to be leveraged at around 3x revenue. This is much healthier than 2021 and probably low enough to service cash interest, but still a large part of the success of these loans will gravitate around finding a successful exit. Non-tech large cap PE buyouts are leveraged at 5-6x EBITDA… Many tech companies have a very thin EBITDA to start with. The average EBITDA/Interest coverage ratio of private credit transactions in all sectors is 2x, which already indicates notable refinancing risk. Tech is probably much lower.

So, up to now, we know things went wrong 5 years ago but not enough to derail private credit. We also sense more things may have gone wrong in recent years, but it is harder to tell now. One interesting thing about these quasi-equity-risk loans is the way they are structured: bullets or limited repayments; PIK interest or elective cash/PIK interest; covenant-lite; in summary, little debt service through their life. Therefore, the way to measure the health of the loans is by measuring the health of the borrowers rather than attesting debt service metrics. Valuation methodologies are somewhat obscure. There are some guidelines by the FASB and IASB, there is also SEC’s rule 2a-5 for US managers, and these revolve mostly around:

Predicted cash flows based on current market interest rates, and

Fair market value of the receivable.

These are ambiguous enough to give wiggle room to fund managers to play with their LPs and auditors in their reports. Take Medallia above, for example. Creditors have marked their position down by 25%, implying they could sell Medallia and recover 5x revenue. Let me be moderately skeptical about that happening in the current market.

A broader question, that would be perhaps material for another article, is this: if private credit has skeletons in the closet, and private credit is leveraging private equity, then how tidy is PE’s closet?

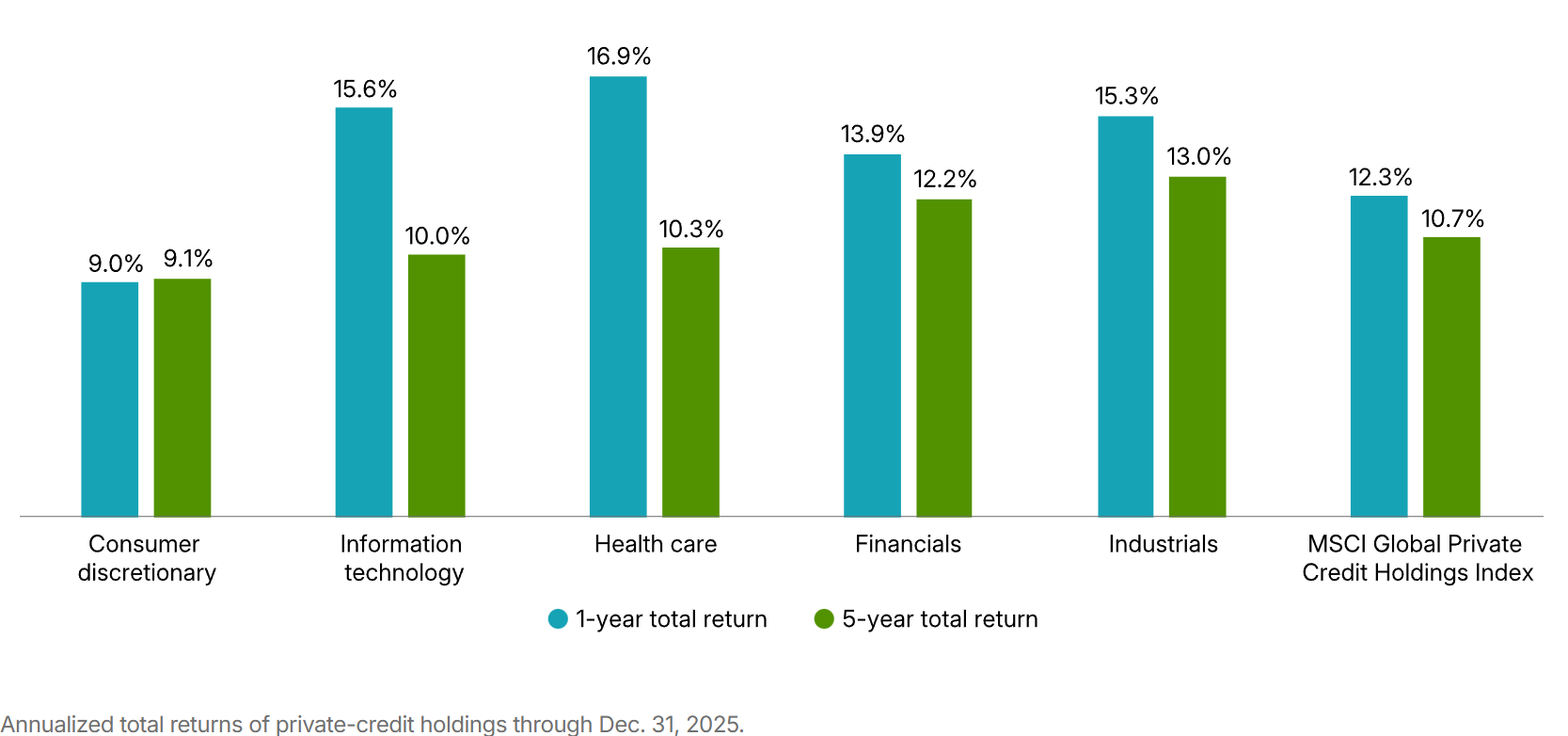

Finally, another important matter: funds use back leverage to amplify their deployment capacity and improve their returns. Around 1/3 of AuM are back leveraged. In general, the back leverage providers should be safe given the relatively low % leverage, but the credit funds will experience more pain because of this policy. Reported returns are around low double-digit now (see below), but I sense many reputable managers will have to declare losses that will likely eat these returns.

What can happen to the overall economy in a private credit meltdown scenario?

Ok, so private credit will have to purge a few years of exhuberance. Is this doomsday?

There is nothing new under the sun. Take the demise of Credit Suisse two years ago and its conversion into Atlas. Credit Suisse had been the high yield specialist since the acquisition of DLJ 25 years ago, and left a $500Bn hole when it died. It was a big, yet manageable hit. Let’s not talk about Drexel’s role in the 1980’s high yield bond industry. Investments gone wrong are not very problematic if they are carried out by closed fund structures and no deposit holders are involved. Don’t expect governments bailing out private credit funds.

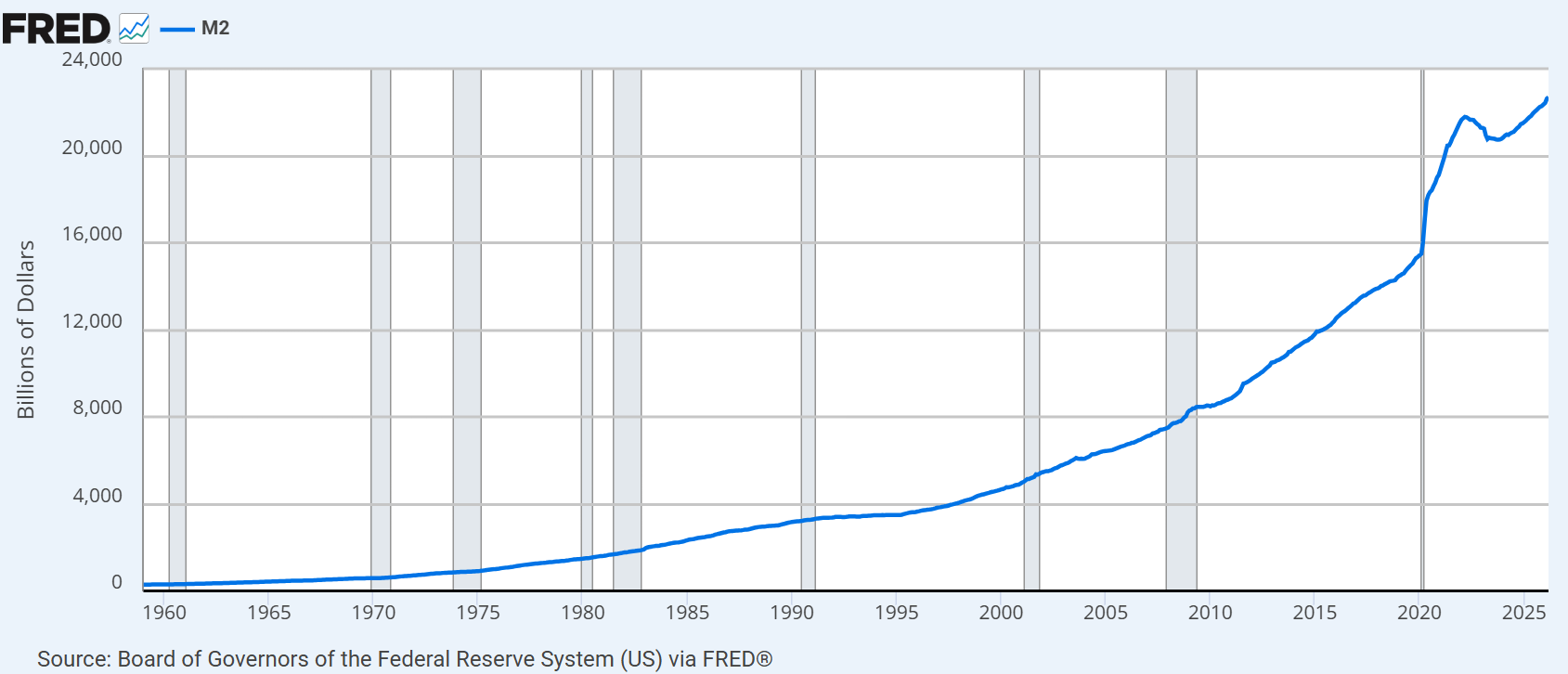

Furthermore, given there is close to $1Tn dry powder to be deployed in the coming years, fund managers still have an opportunity to redeem themselves with tighter policies and blame it on a bad cycle, and top quartile fund managers will take market share from the worst ones. Global liquidity is at its peak (M2 USD below) and still growing, and close to 10% of USA’s population are millionaires, so investors will double down under the promise of 10% yields.

Source: https://fred.stlouisfed.org/series/M2SL

What may be sadly true is that a big number of retail investors and some government entities will experience losses. Behind these fund managers is a ladder of investment vehicles that go up to pension funds and institutions such as the European Investment Bank. That being said, a 50% loss on private credit would amount to only to 1-2% of global liquidity, so it is a hit we can absorb. These losses may however trigger higher scrutiny from regulators and require more granular and accurate valuation policies.

How will the tech industry be affected?

The policy of funding a maximum percentage of a buyout is self-adjusting. Market multiples being lower means leverage multiples automatically being lower. If funds hold to this policy, we will see no particular impact in multiples because of credit scarcity, especially considering the available deployment capacity. Only if funds start leveraging a lower percentage of acquisitions (say, 25-40% instead of 40-60%), valuations will see an equivalent haircut (i.e. around 15-20%).

My prediction is that we will see increased volatility and discrimination between good and mediocre assets. Private equity and private credit funds will continue to partner to buy out best-in-class companies for strong multiples; but they will steer clear of assets with AI-related existential risk or bad SaaS metrics.

Conclusion

So, to summarize, these are my takes:

It is highly likely that there are notable latent losses within private credit

There is no systemic risk in those losses

Private credit will continue deploying under slightly modified policies unless regulations either open banking again (unlikely) or tighten private credit (more likely, especially on the reporting and valuation side)

Tech valuations may experience some contraction due to modified policies compounding on broader sectorial issues, but this impact will discriminate between good and bad assets